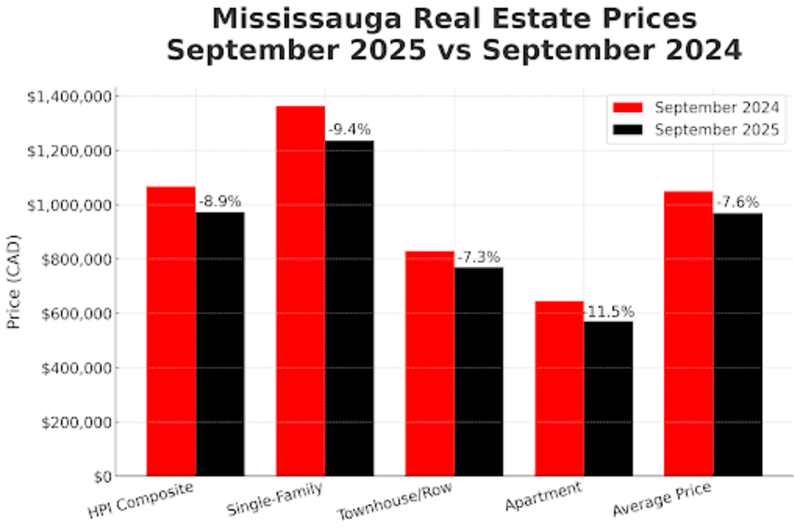

The Waterloo Region housing market in September 2025 reflected a continued move toward balanced conditions, shaped by moderating sales activity and rising supply. Broader economic factors have contributed to a slower pace of transactions compared to both last year and longer-term seasonal norms, giving buyers more time and choice than they have had in previous years. While prices remain below 2024 levels, month-to-month pricing trends indicate some stabilization as the fall market unfolds

Prices

Average sale prices across the region softened compared to the previous year but rose slightly from August, indicating pricing stability at the start of the fall season. The average sale price for all residential properties in September was $753,162, down 4.7% year-over-year (y/y) but up 3.2% month-over-month. Detached properties sold for an average of $858,872, a decrease of 5.9% from last year and up 1.4% from August. Townhouses recorded an average price of $606,871, marking a 1.7% increase year-over-year and 1.8% month-over-month (m/m). Apartment-style condominiums averaged $442,086, a decline of 8.9% annually but an increase of 2.0% from the prior month. Semi-detached homes sold for an average of $621,026, down 5.1% year-over-year and up 0.5% month-over-month.

The Composite Benchmark Price in Kitchener-Waterloo was $673,100 in September, down 7.6% from last year and 0.3% lower than in August. Townhouses saw the sharpest benchmark adjustment, with a 9% year-over-year decrease to $548,300.

Sales

The number of homes sold across the Waterloo Region through the MLS® System in September declined by 4.7% from the same month in 2024, with a 25% decrease compared to the region’s ten-year average for September. The decline in sales has eased the competitive environment that characterized recent years, particularly during periods of constrained supply. With sales volumes lower and inventory higher than last year, buyers generally have more time to make purchase decisions.

The breakdown of activity across property types aligns with the broader moderation. Detached homes remained the most active category with 325 sales, 4.1% fewer than in September 2024. Townhouses saw a 5.2% decline y/y, while condominium apartments recorded a 13.6% annual decrease. Semi-detached homes were the only category to see an annual uptick, rising 6.3%.

Inventory Growth and Time on Market

Inventory levels expanded significantly compared to both last year and long-term norms, which has played a central role in balancing market conditions. A total of 1,469 new listings were added in September, representing an 11% increase year-over-year and nearly one-third higher than the ten-year historical average. Active listings reached 2,094 by the end of the month, marking a 22.2% annual increase and standing nearly 80% above typical September levels seen over the past decade.

The increase in supply translated into a 4.0-month inventory level across all property types. Condominiums demonstrated the largest supply buffer with 7.3 months of inventory, followed by townhouses at 4.8 months and detached homes at 3.3 months.

Regional Resilience

Despite the moderation in pricing and sales, the foundations of the Waterloo Region market remain strong. The region continues to benefit from a diversified economic base, including its established technology sector, higher-education institutions, and skilled labour pool. These long-term fundamentals support steady housing demand even when short-term conditions shift.

The shift toward balance reflects higher supply and more moderate demand, rather than a clear downturn. With inventory elevated, conditions have steadied, resulting in a slower and more measured market pace than during the tighter periods seen in recent years.