According to the March 2024 Edge Report, current trends in debt service ratios and net worth may indicate areas of concern. The prevalence of static payment variable rate mortgages, household debt-to-GDP ratios, and Canada’s heavy reliance on real estate assets, may raise concerns about resilience.

Debt Service Ratios

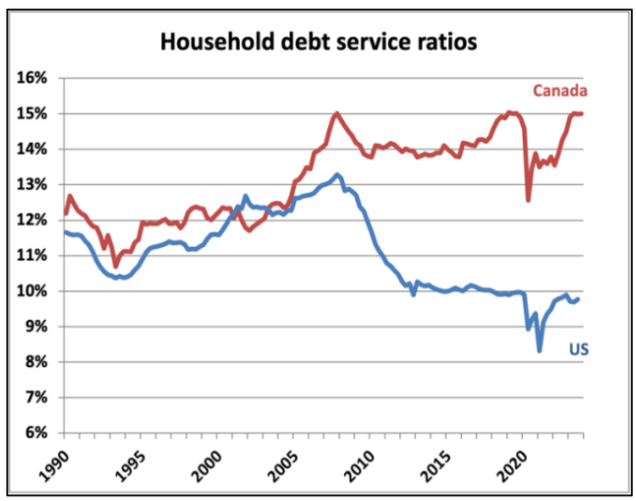

In Q4 of 2023, debt servicing costs stayed stable, with the household debt service ratio holding steady at 15%. This ratio, which reflects the portion of disposable income allocated to debt repayment, remains significantly high, at levels not seen since 1990. A minor adjustment downwards from the previously reported peak of 15.2% in Q3 should be noted, however.

Source: Edge Realty

The low levels of the debt service ratio may be attributed to the continuous decrease in mortgage principal repayment, which reached its lowest point in sixteen years during the last quarter. This trend is driven by the prevalence of static payment variable rate mortgages, which make up nearly a quarter of all outstanding mortgage balances in Canada. These mortgages, only found in Canada, provide consistent payments throughout the mortgage term, adjusting the amortization period as interest rates fluctuate. However, this strategy comes with a caveat: upon renewal, typically after a five-year term, the amortization period reverts to its original schedule. This can potentially result in a substantial increase in payments, which can come as a bit of a shock to homeowners.

According to the BOC, as of 2022, variable mortgage rates accounted for about a third of total outstanding mortgage debt, an increase from about 20% at the end of 2019. About 75% of these have static, or fixed payments.

Debt-To-GDP

Canada’s household debt-to-GDP ratio was 102.5% during Q4, dropping from its peak of almost 112%. This makes Canada one of only a few OECD nations where household debt exceeds the 100% of GDP threshold, posing an ongoing risk if interest rates remain at higher levels.

However, it’s important to note that Canadians have significant assets to offset these debts. As of Q4, $6.55 in household assets back every dollar of debt; this is slightly lower than the peak in 2021, but higher than levels observed a decade ago.

This is partially due to high levels of homeowner equity in Canada compared to the United States. Canadian homeowners maintained an average of 75% equity in Q4, a full five-point lead over their American counterparts. However, this figure is skewed and increased because of the large number of Canadian homeowners – nearly half – who have no mortgage debt.

Source: Edge Realty

Net Worth

In Q4, household net worth increased by 1.8%. This increase counteracted the 1.8% decline witnessed in the preceding quarter. The rise in net worth was predominantly attributed to the robust performance of capital markets, with the value of financial assets held by households rising 5.0% during the quarter.

Source: Edge Realty

However, despite this positive trend, overall net worth is still 2.5% below peak levels. Although this seems a small amount, it’s important to note that we are in the ninth consecutive quarter of a negative trend for balance sheet indicators. Notably, over the past 30 years, there hasn’t been a precedent for such a prolonged downturn. Furthermore, there is a well-documented trend where balance sheet recessions have a prolonged impact on consumption habits. Through the “wealth effect”, when people perceive they have diminished wealth, they tend to curtail their spending, creating ongoing negative impacts on economic growth which can last for extended periods past the original period of recession.

Real estate assets further decreased by 1.8% in Q4, building upon the 1.5% decrease observed in Q3. Nevertheless, these assets still account for nearly 300% of the country’s GDP, which is twice the proportion seen in the United States.

Source: Edge Realty

This situation highlights Canada’s susceptibility to continued declines in real estate values. Policymakers will be aware of these risks. However, some experts feel that this situation also suggests the economy may be weaker and more fragile than commonly perceived, and that the Bank of Canada will likely need to deal with this issue in the near future. As a result, the Edge Realty report forecast predicts a total of 150 basis points of rate cuts throughout the year.