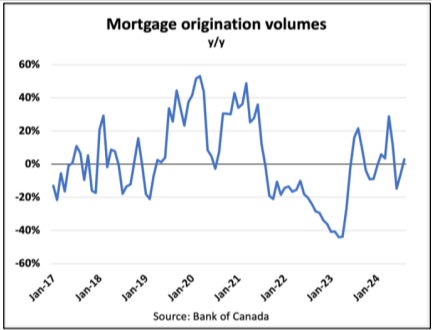

Mortgage origination activity showed an increase in August, with a 3% year-over-year (y/y) rise in demand driven largely by a surge in variable-rate products. These products saw an impressive 85% growth y/y, though they still make up only 10% of the overall mortgage volume. The majority of new originations still favoured three- to four-year fixed-rate options, accounting for 55% of total volumes.

According to an Edge Realty Analytics October 2024 report, there has been a substantial increase in mortgage inquiries and pre-approvals, signalling that many Canadians are positioning to enter the market. If this momentum holds, it could translate into further mortgage and home sale activity through the remaining months of the year, suggesting a potential seasonal upswing in an otherwise moderating market.

Source: Edge Realty Analytics

Impact of OSFI’s Loan-to-Income (LTI) Limits

As mortgage demand rises, regulatory changes from the Office of the Superintendent of Financial Institutions (OSFI) are also set to influence the market. Starting November 1, OSFI will implement a new loan-to-income (LTI) limit, which caps the number of high-LTI mortgages lenders can originate to only 15% of their total mortgage volume each quarter. This measure, intended to curb potential risk concentration, limits new loans with LTIs above 450% of borrower income—a level some in the industry believe could dampen speculative booms seen in past market cycles.

Peter Routledge, OSFI’s Superintendent described the cap as an “effective ceiling that stops the build of risk concentration.” OSFI had initially proposed limiting these higher-LTI loans to between 20% to 30% of volume; however, this final cap of 15% marks a stricter stance on lending leverage. For example, during recent housing booms, loans exceeding the 450% LTI threshold comprised up to 26% of new mortgages.

If OSFI maintains this limit, it would restrict Canadians’ ability to take on significant leverage even if interest rates decline in the future. Additionally, there is industry speculation that if this LTI cap becomes standard, OSFI might reconsider the stress test, potentially relaxing it as the stricter LTI measure takes effect. This would represent a notable shift, as the LTI ceiling would already serve as a strong check on excessive borrower leverage.

While OSFI’s attention has been directed toward managing mortgage leverage, Ben Rabidoux of Edge Realty Analytics suggests that consumer credit issues in other areas may pose a growing risk to consider. Credit card debt, for instance, rose another 0.7% nationally last month, accelerating at roughly three times the pace of lower-interest mortgage debt. This trend suggests that, as OSFI aims to manage risk in mortgage lending, rising consumer debt in higher-interest categories like credit cards may warrant closer scrutiny.

Bank Responses

Responses from major banks to recent regulatory changes and the evolving mortgage environment have been varied, with some institutions adapting well while others scale back. This indicates a segmented market where individual bank strategies and risk profiles significantly influence their mortgage lending patterns.

Modest Mortgage Growth Amid Rising Incomes

While originations rose in August, overall residential mortgage growth remains limited at 3.5% y/y, which is only about half the pace of aggregate household disposable income growth. This slower mortgage expansion compared to income growth indicates a de-leveraging effect as Canadians take on new debt at a more cautious rate than they increase their incomes. As the LTI restrictions are expected to limit leverage further, it will be crucial to monitor how borrowers and lenders adapt to this tightened regulatory environment.