Recent inflation data may have been misleading, but there have been other signs of an economic slowdown, evidenced by two disappointing employment reports in the past few weeks, according to a July Edge Realty Analytics report.

Employment Decline and Rising Layoffs

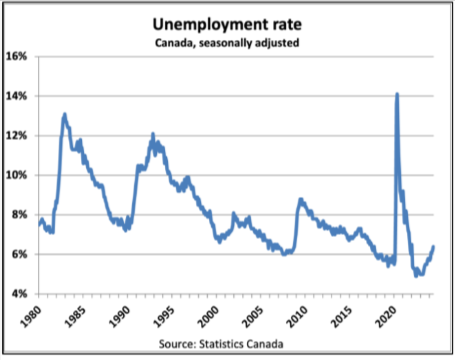

First, the Labour Force Survey reported a month-over-month decline of 1,000 jobs in June, far below the expected gain of 25,000. This drop was driven by a 20% year-over-year increase in layoffs, rather than weak job creation. Strong population growth combined with soft employment trends pushed the unemployment rate up by 0.2 percentage points to 6.4%, marking a 1.6 percentage point increase from post-pandemic lows—already a larger rise than in several historical recessions over the past 30 years.

Sector-Specific Job Losses

Job losses were notable in key cyclical industries such as transportation (-11,000), retail/wholesale trade (-10,000), and construction (-4,000). Conversely, accommodation and food services saw an increase of 18,000 jobs. Construction employment has now declined for three consecutive months, down nearly 3% in total—a pattern previously seen only during significant economic downturns in 2020, 2009, and the early 1990s.

Source: Edge Realty Analytics

Housing and Construction Employment Outlook

The Edge report predicts that housing starts will drop sharply due to the dual impact of slowing condo starts, given the normal lag between preconstruction sales and housing starts, and the tightening of the MLI Select CMHC rental development financing program. This will likely exert further downward pressure on construction employment, historically a precursor to broader employment declines in interest rate-driven recessions.

Source: Edge Realty Analytics

Impact on Hours Worked

Over the past three months, job gains have been concentrated in part-time employment, with full-time positions declining by 4,000 in June and 39,000 over the past two months.

Source: Edge Realty Analytics

Hours worked, a critical factor for the Bank of Canada as this metric is a direct input into GDP, declined by 0.4% in June and are up just 1.1% year-over-year, despite a 3% population growth. Canada’s labour market is struggling to keep pace with this rapid population increase, with the employment rate dropping by 0.2 percentage points, falling below the lows seen during the Global Financial Crisis.

Source: Edge Realty Analytics

Note: Unemployment rate: The percentage of active job seekers who are unemployed.

Employment rate: The percentage of the total population, including those not in the labour force (e.g., retirees), that is employed.

Payroll

Payroll data indicated a decline of 26,000 positions nationally in April, with a downward revision of March numbers (42,000 from an initially reported 51,000). While the Labour Force Survey had reported a 90,000 increase for the same month, the Edge report notes that historically, payroll data is considered a more reliable indicator when discrepancies arise.

Private sector payrolls fell by 28,000, the steepest decline since the public health lockdowns in 2021, likely drawing the Bank of Canada’s attention.

Source: Edge Realty Analytics

Wage growth slowed to 3.7% year-over-year from 4.1%, with fixed-weight wages increasing just 0.1% month-over-month and 2.8% year-over-year, effectively flat in real terms. Job vacancies also dropped in April, down 13% over two months, marking the steepest decline since 2015, when this dataset first began, and nearly 30% below year-ago levels.

Source: Edge Realty Analytics

Small Business Delinquencies Rise

New data from PayNet, an Equifax company, reveals a sharp increase in small business loan delinquencies in Canada as of April, with 90+ day delinquencies surpassing the levels seen during the Financial Crisis highs.

While partly driven by the start of CEBA loan repayments, which started in January, this trend is corroborated by rising insolvencies and a significant contraction in the number of active businesses, the second-largest since the COVID lockdowns.

Source: Edge Realty Analytics

Considering the misleading inflation reading, a deteriorating job market, and increasing pressures on businesses, it seems unlikely that the Bank of Canada will remain passive. The forecast in the Edge Realty Analytics report is that there will be rate cuts at every BoC meeting for the rest of the year.